Tips to weather the impact of rising home and auto insurance costs

by Kayte Fredrickson

Vice President, OMA Insurance

If you’ve insured a home or car for 10 years or more, you’ve likely noticed that insurance costs more than it used to. Even good drivers and responsible homeowners have seen their premiums go up. Is it you, or is something happening on a larger scale?

Your claims history affects your premiums, of course, but the biggest factors these days are ones affecting the entire insurance marketplace. Distracted driving, especially texting, has led to more crashes. Advanced automotive technologies make even seemingly simple damage, like a dented bumper, more expensive to repair. And most significantly, a rapidly warming climate is causing many more weather-related catastrophes leading to property damage.

For insurance companies and their customers, all these changes have combined to create a perfect storm of events leading to higher costs industry-wide. The good news is that there are ways to mitigate these costs by protecting yourself from events that could lead to claims. There are even apps you can use to help protect yourself from devastating storms and flooded basements. The first step is to understand how premiums are calculated and the factors that drive up costs.

“Weather events are becoming more severe and more damaging than we’ve experienced in the past,” explains Paul Douglas, Senior Vice President of The Personal Insurance Company, group home and auto insurance providers for OMA Insurance. “Over the past five years, there have been a number of high-level catastrophes, like the Fort McMurray wildfires, and hail and flooding, that have impacted regions right across Canada.”

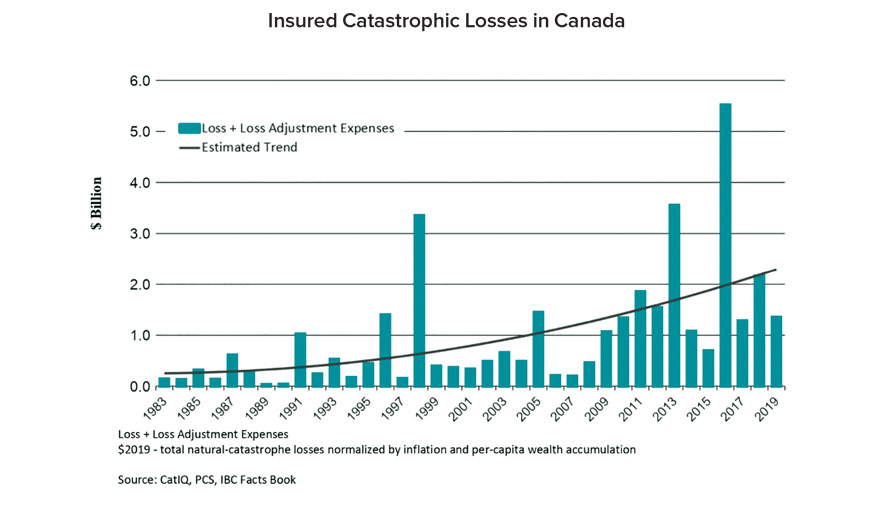

In insurance parlance, a catastrophic loss (known as a “cat”) is an event that results in losses of $1 million or more. Between 1983 and 2008, the average catastrophic loss was approximately $400 million per year. Over the past decade, the average cat loss has jumped close to $1 billion per year, and almost $2 billion in the last year alone.

“Severe weather claims paid by insurers could almost double over the next 10 years, according to the Insurance Institute of Canada,” says Douglas. “Last spring, Environment and Climate Change Canada (a branch of the Government of Canada that tracks climate change) issued a report saying that Canada is warming twice as fast as the global average. When you have a warmer climate, temperatures become more extreme. The result is a huge impact by weather on property claims.”

The risk of flooding is especially severe, with 50% of all property claims caused by intense rainfall and hailstorms leading to flooding. That can be especially damaging to houses with finished basements. “On average, a basement flooding claim costs $43,000 to fix. That can be quite an extensive claim – electrical, flooring, and so on,” explains Douglas.

Insurance companies not only have to manage the rising costs of claims caused by property damage, but the cost of insuring themselves. “Insurance companies are insured by reinsurance companies, something most people don’t know about,” says Douglas. “Reinsurance premiums and deductibles have skyrocketed over the past five years. That’s a cost an insurance company has to handle.”

Auto insurance, too, is impacted by factors that go far beyond an individual driver’s personal accident history. One of the biggest factors is the prevalence of distracted driving. Whether that means talking on a phone, texting, eating, checking a GPS or even sipping coffee, when a driver is not fully focused on the road, the chance of a collision rises dramatically.

Douglas notes the statistics illustrate the scope of the problem: “According to a survey done by the Traffic Injury Research Foundation, driving fatalities from distraction in some parts of Canada exceed those caused by impaired driving. Texting while driving makes a driver 23 times more likely to be in an accident than someone paying attention to the road. It accounts for four million car crashes a year in Canada.”

Cars have also become much more technologically sophisticated, which in turn affects the cost of repairing them. Damaged infotainment systems, sensors, cameras and LED lighting can all be expensive fixes. Even basic automotive parts, such as airbags, windshields and bumpers, require more specialized equipment and a more skilled and knowledgeable technician to make repairs.

“Bumpers in the past might have cost a couple of hundred dollars to repair,” explains Douglas. “Today, bumpers are full of technology – such as cameras, radars and lasers – and they’re also connected to air bags. A little dent in a bumper could impact the car’s entire navigation system. Windshields now have sensors for automatically running windshield wipers. More modern air bags contain sensors programmed to the height and weight of people in the front seats.”

All these technological tools increase the cost of repairs, even when it’s just a so-called “fender bender.”

With all these factors in mind, what can you do to control premiums? According to Douglas, a good first step is to talk to your insurer before you buy a car or move to a new neighbourhood.

“We recommend that when someone is shopping around for a new vehicle, they should first phone their insurance company to get a ballpark quote. The premium is based on actuarial data – historical claims for cars already out there, the frequency the vehicle has been involved in an accident and the injuries that resulted.”

The same holds true for property insurance: “There are charts of areas where people live that help you see whether it’s on low-lying ground (thus making the property more flood prone). Working with your insurer can help you get a better picture of the premium you will have to pay.”

Another tip for property insurance is to do an inventory of the valuables you have in your house and check whether they require special insurance. For example, jewelry, works of art, computers and even cash could require special riders, or an umbrella policy that includes coverage for the types of valuables you keep in your home.

The Personal was one of the first insurance companies to launch mobile apps designed to help their customers mitigate damage to themselves or their property. Their RADAR App sends out alerts before major storms, giving you time to protect property and yourself. The ALERT App is a sensor placed in areas of the home where there’s the potential for rising water, such as sinks and showers. “We look for ways to proactively help our customers,” says Douglas.

As an OMA member, you, your family and medical staff are eligible for exclusive home and auto insurance rates through The Personal. As the group insurer for OMA Insurance, The Personal offers members ways to save, including by bundling home and auto insurance together. For more on OMA Home and Auto Insurance, visit the OMA Insurance website.

For more details about OMA Insurance solutions that protect you and your practice, visit the OMA Insurance website, or call 1.800.758.1641 to speak to an OMA Insurance advisor.